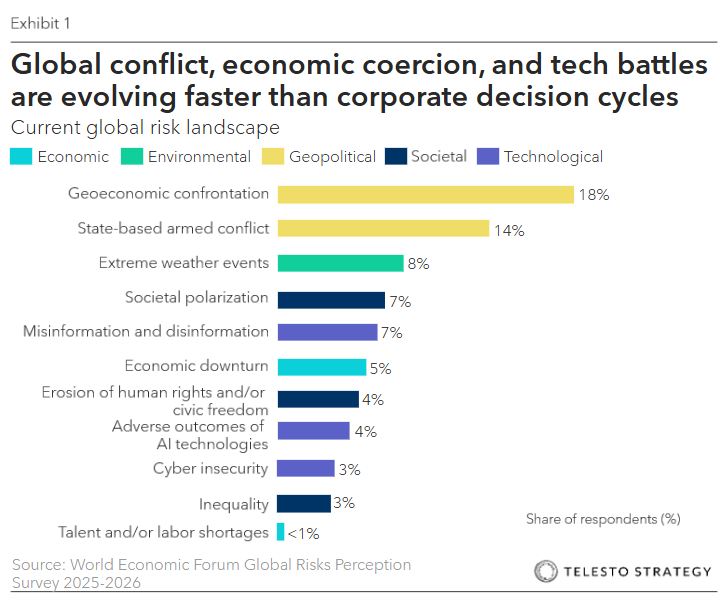

In 2026, geopolitics no longer simmers in the backdrop; instead, it should be considered a design constraint for growth, capital allocation, and operational continuity. As opposed to thinking about which conflict is most likely to erupt, leaders will have to understand which stack of pressures will compound fast enough to break our assumptions. The World Economic Forum’s 2026 Global Risks Perceptions Survey puts geoeconomic confrontation (e.g., tariffs, investment restrictions, resource leverage) as the top short-term risk, now overtaking armed conflict. The central question worth exploring – can your firm absorb shocks without halting growth?

Key takeaways:

- Geopolitics, and how enterprises assess their risks and opportunities, has shifted from “where we operate” to “how we compete.”

- The highest impact scenarios are great-power adjacent — Tawain as well as Russia-NATO clashes.

- Risks will be coupled and compound in magnitude; most companies are underprepared and highly exposed to geoeconomic shocks.

- Boards will need to shift from risk register oversight to adaptive and integrative governance.

2026 will be a year of coupled risks, be it regional flashpoints, economic coercion, and technology contestation interacting faster than corporate decision cycles. The winners, thus, will be firms that treat geopolitical volatility as an enterprise capability (e.g., through scenario design, contractual resilience, compliance agility, and supply chain optionality), not a quarterly risk memo.

As boards members seek training and improved readiness on the highly nuanced and complex geopolitical landscape, we offer watch items for 2026.

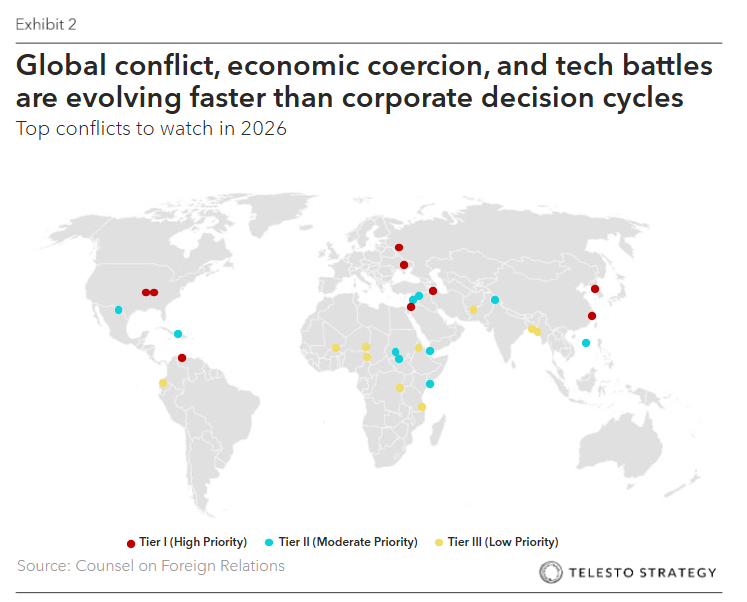

Telesto Strategy is closely monitoring the changing geopolitical environment; we see the following as the flashpoints to watch as we start 2026:

1. Taiwan Strait

- State of play: The pressure in the Taiwan mounts, intensified by Chinese military, economic, and political pressure on Taiwan. Beijing continues to use large-scale joint drills, both air and maritime activity around Taian, and demonstrations that resemble potential blockade or quarantine playbooks. Late December 2025 drills were described as China’s most extensive war games to date.

- Board lens: Requires deeper analysis on what revenue, supply, and critical vendors are Taiwan-coupled directly – or through – Tiers 2-3. Prepare a business resilience scenario for a blockade, where Taiwan is cut off from outside support and its ports are shut down.

2. Russia-Ukraine and NATO escalation pathways

- State of play: Leading think tanks anticipate intensified attacks on critical infrastructure and population centers as a high-likelihood, high-impact scenarios. Elevated risk of armed clashes between Russia and one or more NATO member. At the same time, diplomatic activity increases, yet outcomes are uncertain and contested.

- Board lens: Expect continued energy price volatility, cyber spillovers, sanctions expansion, and transport disruption in Europe. Sanctions and export-controls from the EU, UK, and U.S. will continue, continuous monitoring will be necessary. Confirm and codify evacuation support, insurance coverage, and HR legal contingencies.

3. Israel-Gaza, broader entanglement with Iran

- State of play: The Council on Foreign Relations lists heightened conflict in the West Bank and renewed fighting in Gaza as high-likelihood, high-impact, with the possibility of renewed Iran-Israel conflict linked to nuclear and proxy-network dynamics.

- Board lens: Regional escalation affects aviation routes, shipping insurance, energy risk premia, and compliance.

4. Red Sea and Suez reliability

- State of play: The Red Sea remains volatile and critical to business operations; with security risk easing from peak levels, major logistics companies have reintroduced transit through the Red Sea and Suez Canal. Suez traffic has recovered only partially, with Egypt offering incentives to revive volumes after a steep drop tied to attacks and rerouting around the Cap of Good Hope. The U.S., in the backdrop, continues to target Houthi enabling networks, which signal an ongoing concern about financing and logistics used for maritime attacks.

- Board lens: Assess contractual levers (e.g., indexing, surcharges, force majeure clarity) and whether inventory strategy anticipates route volatility. Treat both corridors as operating systems risks. Clarify policies for war risk insurance, approved routing, and voyage governance as applicable directly or indirectly to business operations.

5. U.S. expanding its military activity in the Western Hemisphere

- State of play: Some analysts have already introduced the “Donroe Doctrine” of U.S. leadership and its sphere of influence in the Western Hemisphere. With interventionist actions in Venezuela and language towards Greenland, traditional allies in Latin America and Europe may be excluded or estranged. Greenland’s vast resource wealth and strategic geographical positioning have put it front and center.

- Board lens: Evaluate operational risks in the Caribbean and EU, given escalating political risk and trade tensions.

6. South China Sea coercion risk with alliance entanglement

- State of play: Beyond Taiwan, Chinese aggression can expand throughout the region to Philippines, which would entangle the U.S., the Quad, and other allies. Watch for a U.S.-China deal, with Presidents Trump and Xi set for as many as four summits over the course of 2026. Both sides have incentives to keep whatever stability in their relationship, even if fragile. Yet, both countries need to address fundamental, structural points of friction, including U.S. technology restrictions and support to Taiwan. As a secondary effect to the U.S.’s expansionist policies in its region, China may call for legitimization of their expansionist efforts in the South China Sea.

- Board lens: Evaluate exposure in logistics and Tier 2-3 suppliers in the region.

7. North Korea nuclear testing

- State of play: If North Korea resumes its nuclear tests, response may include an armed confrontation involving regional powers. In early January, North Korea test-fired hypersonic and ballistic missiles, which state media and neighbors reported as significant weapons drills and increasing regional tensions.

- Board lens: Monitor for sudden sanctions adjustments, shipping/insurance restrictions, and regional security posture changes affecting Korean and Japanese operations.

8. AI-enabled cyberattack on critical infrastructure and governance

- State of play: Experts warn of the risk of highly disruptive, AI-enabled cyber-attack on critical infrastructure as moderate in its likelihood. Similarly, WEF elevates concerns about AI governance and longer-horizon systemic risk. 94% of business leaders identify AI as the primary driver of cybersecurity change in 2026 and 64%

- Board lens: Treat cyber not just as an IT risk, but as operational continuity and safety risk — especially for energy, logistics, healthcare, manufacturing, and finance.

9. Sudan and wider African instability

- State of play: Escalation of existing conflict likely, with risks of mass atrocities and spillover effects into neighboring countries. With Sudan at the epicenter of conflict, a clash between two of its neighbors, Ethiopia and Eritrea, could tip the Horn of Africa into all-out confrontation.

- Board lens: Regional instability may disrupt critical minerals and agricultural flows; additional visibility and contingency options required.

10. Geoeconomic confrontation through tariffs, outbound investment rules, and sanctions expansion

- State of play: Ranked as the top global risk in 2026 by WEF, we find ourselves in a world where trade and investment policy become a primary lever for geoeconomic confrontation.

- Board lens: Trade policy fluctuations and uncertainty will continue to drive P&L, principally through market access, cost of capital, sourcing, and enforcement exposure. Scenario planning, stress-testing, and reversibility will all be table stakes capabilities.

Actions boards can take:

- Reframe geopolitics as an enterprise capability. Establish a standing operating rhythm with monthly risk briefs, quarterly scenario drills, and a management “early warning” dashboard tied to decisions required on inventory planning, sourcing, pricing, capex timing, logistics

- Map “coupled exposure,” not just country exposure. Require management to quantify: (a) revenue risk, (b) supply at risk (inclusive of Tiers1-3), (c) logistics chokepoints dependence, (d) regulatory/compliance fragility

- Build contractual resilience as a strategic asset. Upgrade force majeure language, freight and energy indexing, supplier step-in rights, dual sourcing clauses, and data localization provisions where relevant

- Stress test the company’s “permission to operate.” Sanctions, export controls, and investment restrictions are moving targets; ensure auditability of end-use, beneficial ownership screening, and third-party risk controls

Questions for the boardroom:

- What is our top “coupled risk” scenario for 2026 and what do we do in the first 72 hours?

- Where do we have single points of failure in Tiers 2 and 3 in our supply chains or our cloud and network connectivity?

- What portions of our earnings is exposed to trade policy swings? Who owns that to ensure operationally?

- Do we price geopolitical risk appropriately?

- What are management’s leading indicators and what decisions are they tied to?

Additional Telesto resources:

- BoardCollective by Telesto is where current and aspiring corporate directors learn to lead on sustainability

- Board series: The Board Chair of 2026: From strategy steward to enterprise risk

- Market intelligence enables executives to win in market and capture more value by understanding trends, customers and competitors

- Prism, our ESG benchmarking tool, helps your organization to rapidly strengthen its Sustainability, Climate, and ESG performance and disclosures through in-depth benchmarking of industry peers and identification of gaps and areas of distinction

Let us show you how we can move your board from risk oversight to adaptive governance that protects growth.