African banks are standing at the edge of a historic capital reallocation. Climate finance flows to emerging markets are accelerating, yet they remain highly concentrated in a small set of countries and institutions. The constraint is no longer a lack of capital — it is institutional readiness. African banks that cannot demonstrate credible emissions baselines, disciplined reduction pathways, and defensible impact measurement are increasingly sidelined from green capital flows, regardless of ambition or intent. For domestic leaders, the opportunity is clear: elevate sustainability architecture to global standards and position the institution as a trusted regional conduit for climate finance.

Key takeaways:

- Climate capital follows credibility, not aspiration. Without globally aligned emissions baselines and impact reporting, banks are excluded from the fastest-growing pools of green finance.

- Operational emissions are the entry point, not the end state. Scope 1 and 2 rigor is now table stakes for accessing sustainable capital and issuing green instruments.

- Impact without measurement is a liability. Weak impact analysis exposes institutions to greenwashing risk, regulatory penalties, and reputational damage.

- Regional leadership is built in phases. Institutions that sequence readiness — first nationally, then regionally — are best positioned to capture outsized capital flows.

The Capital Is there. The readiness is not.

Africa’s share of global climate and green finance is estimated at approximately $14 billion annually, with flows concentrated in South Africa, Egypt, Kenya, Nigeria, and Morocco. Zambia — and much of Southern Africa — lags not because of insufficient demand or opportunity, but because fewer institutions meet the reporting, governance, and disclosure thresholds now expected by international capital providers.

Global investors, DFIs, and regulators increasingly require alignment with ISSB/IFRS Sustainability Standards, TCFD-consistent climate risk management, and credible emissions accounting methodologies before deploying capital.

This shift mirrors trends observed by the Network for Greening the Financial System (NGFS) and the International Finance Corporation (IFC), which have repeatedly emphasized that financial institutions are transmission points — not passive participants — in the low-carbon transition.

How are regional banks responding?

African banks face a binary choice: advance to regional leadership or be overtaken by faster-moving peers.

Institutions that act decisively can:

- Lead national markets on sustainability and green finance issuance

- Build institutional readiness to intermediate international climate capital

- Establish trusted brands with regulators, investors, and development partners

Those that delay face rising compliance costs, shrinking access to capital, and heightened reputational exposure.

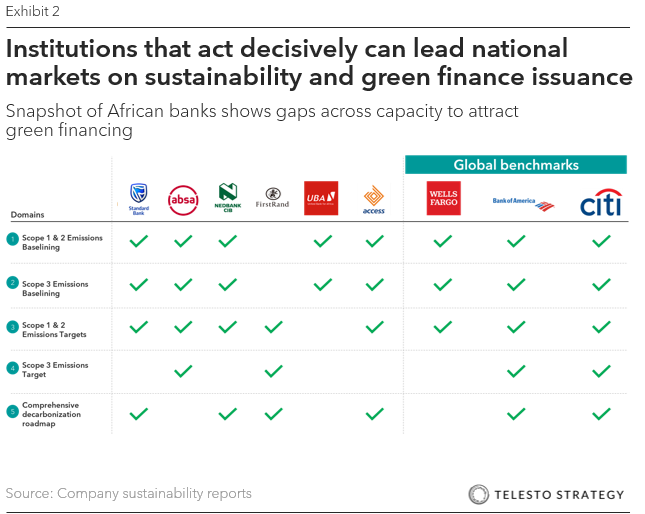

Benchmarking across African and global peers reveals a consistent pattern: many regional banks lack formal Scope 1 and 2 baselines, defined reduction targets, or decarbonization roadmaps, placing them behind global best practice.

Why emissions targets are no longer optional

Banks globally are being pushed — by regulators, investors, and clients — to manage climate-related financial risks alongside traditional credit and market risks. Emissions targets serve multiple strategic functions:

- Enabling access to sustainable finance instruments

- Supporting regulatory compliance across jurisdictions

- Differentiating brand and institutional credibility

- Aligning banking operations with global climate goals

These drivers are consistent with guidance from the ISSB, Basel Committee on Banking Supervision, and European Central Bank, all of which now treat climate risk as a core prudential issue.

Starting where control exists, banks focus on operational emissions

The disciplined approach is to begin with Scope 1 and 2 emissions, where data quality is highest and management control is strongest. This includes:

- Diesel generators and vehicle fleets

- Purchased electricity and grid emissions

- Refrigerants and HVAC systems

This sequencing aligns with the GHG Protocol and Science Based Targets initiative (SBTi) guidance, which emphasize operational emissions as the foundation for credible net-zero pathways.

Furthermore, leading institutions translate emissions targets into capital deployment decisions using carbon abatement cost curves. These tools allow executives to evaluate which interventions deliver the greatest emissions reductions per dollar invested —embedding sustainability directly into capital planning.

This approach is increasingly common among global banks and aligns with transition planning expectations articulated by the Financial Stability Board and NGFS.

Impact without evidence is now a risk

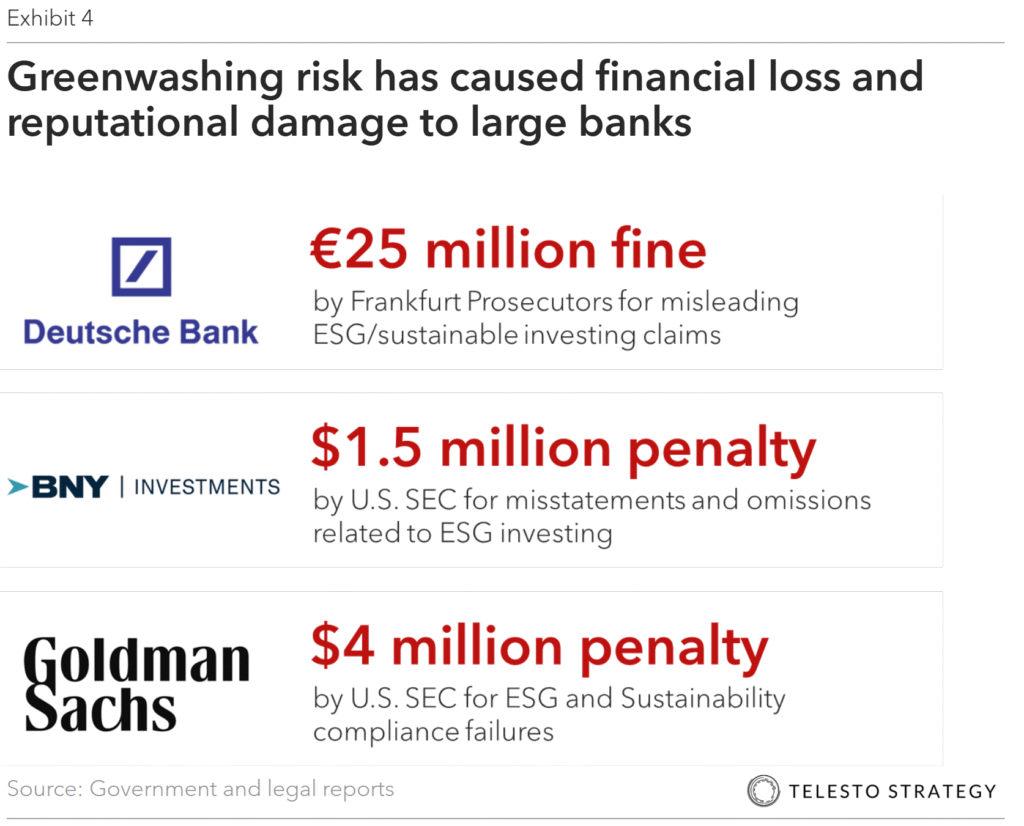

Beyond emissions, banks face growing scrutiny over social and environmental impact claims. High-profile enforcement actions — ranging from €25 million fines in Europe to multi-million-dollar SEC penalties in the U.S. — underscore the financial consequences of weak or misleading ESG disclosures.

For African banks seeking international capital, the implication is clear: impact must be measurable, auditable, and defensible.

Advanced institutions articulate a theory of impact linking inputs, activities, outputs, outcomes, and long-term impact. This framework enables banks to demonstrate how initiatives—from green lending to financial literacy—translate into measurable economic, social, and environmental outcomes. Such models are consistent with methodologies promoted by the World Economic Forum, UN SDGs, and leading development finance institutions.

The strategic payoff—more than compliance

Banks that invest in emissions baselining and impact rigor unlock multiple strategic benefits:

- Enhanced access to international capital – expected to increase from billions to trillions in the next decade

- Improved regulatory resilience across jurisdictions

- Stronger board-level decision-making

- More credible storytelling with stakeholders, avoid greenwashing penalties

Critically, these capabilities position institutions not merely as recipients of climate finance, but as architects of national and regional transition pathways.

The next phase of green finance leadership in Africa will be defined less by ambition and more by execution. Institutions that build rigorous sustainability infrastructure today will shape capital flows for the next decade. Those that delay risk being structurally excluded.

For domestic leaders, the message is simple: institutional readiness is now a strategic asset—and one that compounds over time.

Telesto Strategy — achieving bankable outcomes in the green financing boom

Telesto Strategy is uniquely positioned to support African banks in advancing sustainability priorities and capturing green finance opportunities because it operates at the intersection of global standards, regional realities, and board-level execution. Our approach is tailored and rigorous, one that combines emissions baselining, decarbonization strategy, and impact measurement with deep knowledge of how global capital allocators, DFIs, regulators, and rating bodies assess institutional readiness. Unlike firms that apply “one-size-fits-all” ESG frameworks, Telesto adapts its methodologies to local operating contexts— energy grids, asset mixes, data availability, regulatory environments — while ensuring alignment with international best practice, including ISSB, SBTi, and leading climate finance expectations. This enables African banks to meet global thresholds for credibility without losing strategic relevance to domestic development priorities.

Equally important, Telesto’s value lies in its ability to translate sustainability ambition into bankable outcomes. The firm’s experience across financial services, institutional investment, and public-private climate finance allows it to help banks move from fragmented ESG activities to coherent theories of impact that withstand scrutiny and unlock capital. Through proprietary tools, senior advisory expertise, and a continent-wide expert network, Telesto supports leadership teams in building the governance, data systems, and narratives required to attract international green capital while mitigating greenwashing risk. The result is not compliance for its own sake, but a durable competitive advantage: positioning African banks as trusted intermediaries for climate capital, engines of inclusive growth, and regional leaders in the next phase of sustainable finance.